MediShield Life changes are now moving from announcement to household impact. MOH’s release says the Government accepted the MediShield Life Council’s recommendations to enhance the scheme, with revised benefits and MediSave limits implemented progressively from 1 April 2025 and the outpatient deductible starting from 1 June 2026.

For readers, the headline is not just premiums. The package changes claim limits, introduces an outpatient deductible, and layers in Government support meant to more than offset premium increases for many Singaporeans.

The Date To Know

The outpatient deductible is listed as taking effect from 1 June 2026. That gives households a specific date to keep in mind when comparing older medical-bill assumptions with future claims.

For more practical health explainers, follow our Health & Wellness section.

- Outpatient deductible start: 1 June 2026.

- Revised benefits and MediSave limits: phased from 1 April 2025.

- Government support package: S$4.1 billion.

- MOH says support more than offsets S$1.8 billion in premium increases.

What Households Should Review

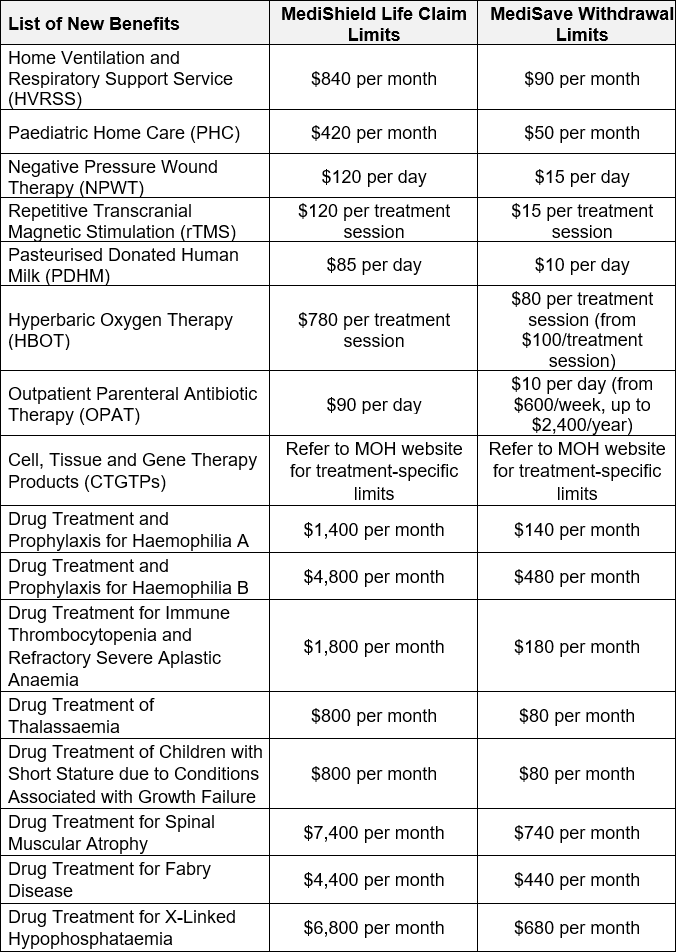

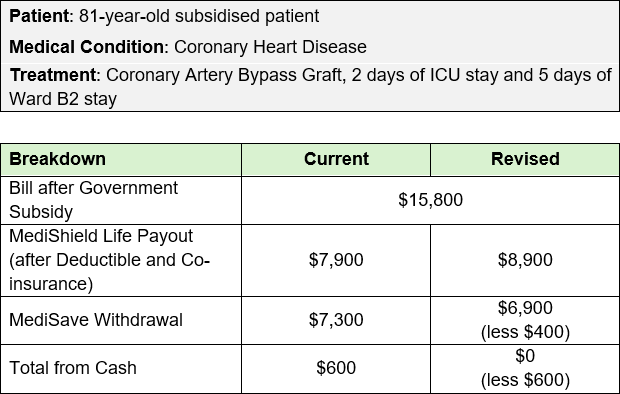

Families should look at three items: current MediShield Life coverage, any Integrated Shield Plan layers, and how much MediSave they expect to use for outpatient or inpatient costs. The tables in MOH’s release are useful because they show where claim limits and support levels are changing.

Older Singaporeans and lower- to middle-income households should pay close attention to premium subsidies. MOH’s release says premium subsidies can go up to 60% for older lower- and middle-income groups.

Why It Matters Beyond Premiums

Healthcare changes often get reduced to premium headlines, but the practical effect depends on the bill type. A household dealing with outpatient treatments will care about the deductible mechanics, while someone planning surgery will look first at claim limits and inpatient support.

The better move is to use the MOH tables as a checklist before a bill arrives: identify the treatment type, understand which MediShield Life limit applies, then ask the hospital financial counsellor how MediSave and any private coverage fit around it.