For many flat buyers, the loan decision is made too late. The useful moment to compare an HDB housing loan and a financial institution loan is before you fall in love with a unit, not after the budget is already stretched.

MyNiceHome’s official housing loans guide, last updated on 13 April 2026, sets out the basic choice: buyers who need financing may apply for either an HDB housing loan or a loan from a financial institution regulated by MAS.

Start With Eligibility, Not Interest Rates

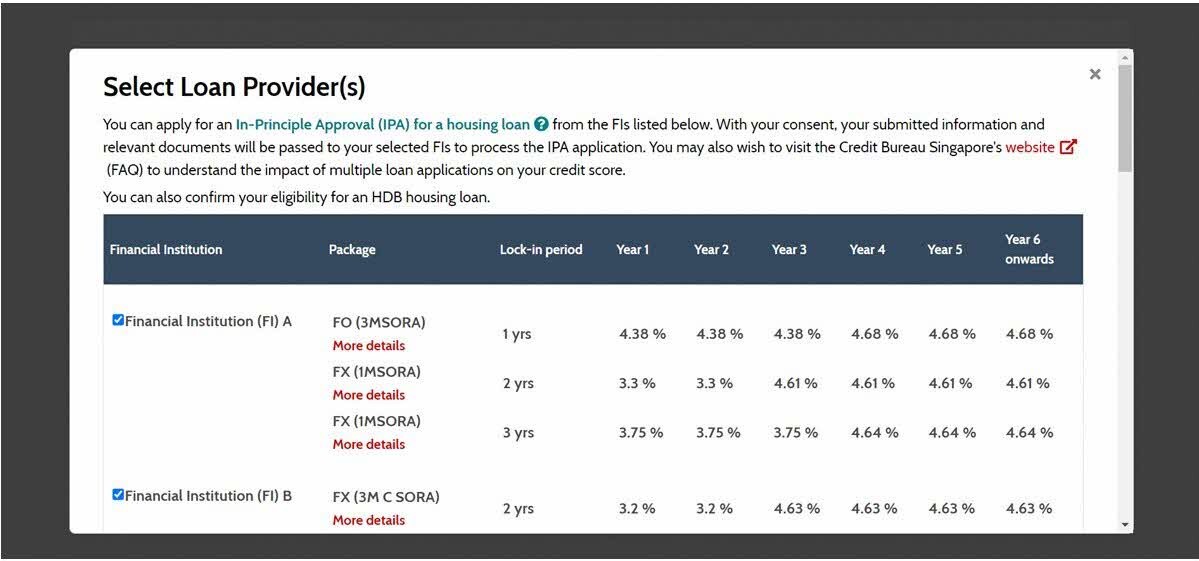

The HFE letter is the first serious checkpoint because it confirms eligibility to buy a flat, CPF housing grants and the HDB housing loan amount you may receive. If you are considering a financial institution loan, MyNiceHome says you may also apply for In-Principle Approvals from participating FIs when applying for the HFE letter.

That turns the HFE stage into a comparison point. Instead of asking only which rate is lower this month, buyers should ask how much they can borrow, how repayments move under different rates and how much cash or CPF buffer remains after renovation and moving costs.

How HDB And FI Loans Differ

The key difference for ordinary buyers is certainty versus market exposure. An HDB housing loan has its own terms and eligibility rules, while a financial institution loan can come with promotional rates, lock-in periods and repricing decisions later.

A lower starting rate is not automatically the best deal if it creates stress when the package changes. Couples should model monthly repayment at a comfortable rate, a higher-rate scenario and a one-income stress case before deciding.

What First-Time Buyers Often Miss

First-time buyers sometimes compare the loan before they have settled the flat type, cash position and grant picture. That can lead to a misleading budget because the affordable purchase price is not simply the maximum loan amount.

The more practical number is the monthly repayment that still lets the household save, insure properly and handle repairs. For resale buyers, it also needs to leave room for valuation differences and renovation decisions.

How This Fits The 2026 Market

Flat buyers watching prices can read LBRD’s URA Q1 2026 private-home price guide for the wider housing backdrop, but HDB buyers should keep the loan decision grounded in household cash flow. A market headline cannot tell you whether your repayment is sustainable.

If you are buying with a partner, compare both loan options with the same assumptions: purchase price, grants, CPF use, cash buffer, possible interest-rate movement and how long you expect to hold the flat.

Official Planning Links

Use the MyNiceHome housing loans guide for the loan comparison, and HDB’s Flat, Grant and Loan Eligibility page for the official entry point into HFE checks. The useful output is not only a loan choice; it is a clearer ceiling on what you can buy without turning the flat into a financial strain.