URA Q1 2026 property statistics give Singapore buyers a clearer read than the earlier flash estimate because the final numbers include the full quarter. The headline is that private residential prices rose 0.9% in the first quarter of 2026, while the private residential rental index rose slightly by 0.3%. That is not a runaway market, but it is also not a clear cooling signal.

URA’s 24 April 2026 release also points to a large supply pipeline, with about 55,800 private housing units, including executive condominiums, expected to be completed in the next few years. URA specifically noted the uncertain macroeconomic outlook and said households should continue to exercise prudence when buying property and taking mortgage loans.

Prices Rose, But Not Evenly

The overall private residential price index increased by 0.9% in Q1 2026, compared with a 0.6% increase in the previous quarter. The important detail is where that growth came from. URA says landed property prices decreased by 0.4%, while non-landed property prices increased by 1.3%, reversing the previous quarter’s 0.2% decline.

Within the non-landed segment, the Outside Central Region posted the strongest quarterly increase at 2.2%. The Core Central Region rose 0.6%, while the Rest of Central Region rose 0.8%. For buyers, that means the broad market number hides different realities depending on whether you are looking at a suburban new launch, a resale condo near the city fringe, or a landed property.

This is why using one national percentage to judge every purchase is risky. A buyer comparing Tampines, Queenstown and River Valley is not really shopping in one market. The URA data is a starting point, but the next layer is project supply, asking-price discipline, quantum and whether recent transactions are genuinely comparable.

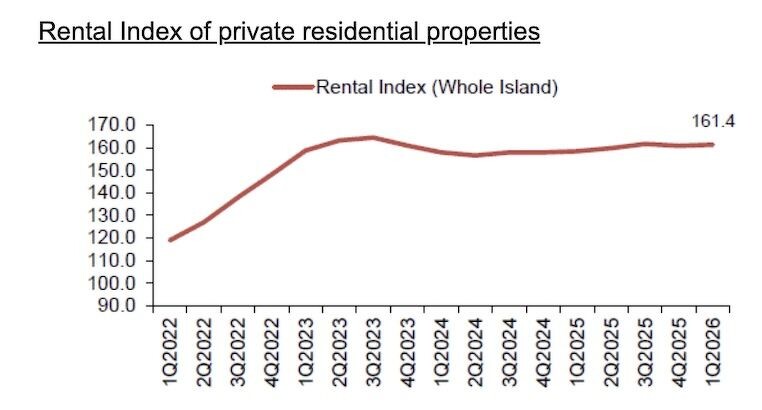

Rents Are No Longer Falling Sharply

The private residential rental index rose marginally by 0.3% in Q1 2026 after falling 0.5% in the previous quarter. URA says non-landed rents increased by 0.4%, while landed rents increased by 0.1%. That suggests the rental market has steadied, but it does not mean every landlord has pricing power again.

Vacancy and completion numbers still matter. If many units enter a particular estate at the same time, tenants may have more bargaining room even if the national index is slightly positive. Conversely, a well-located unit near schools, transport and offices can hold rent better than a headline suggests.

For owner-occupiers, the rent data matters because it affects investors’ willingness to buy and hold. If rental yields stay acceptable, some investors remain active. If financing costs rise faster than rent, the same buyers may become more selective.

Supply Is The Big Moderating Force

URA says about 42,561 units, including ECs, had planning approval at the end of Q1 2026, with 17,032 still unsold. Adding units that have not yet received planning approval, around 30,300 units could be made available for sale later this year or next year. That is a meaningful buffer for buyers watching new launches.

The completion pipeline is also substantial. URA says around 55,800 private housing units are expected to be completed in the coming years, including about 27,300 by 2028 and about 28,500 from 2029 onwards. More supply does not automatically reduce prices, but it can reduce fear-of-missing-out pressure if buyers believe there will be more choices ahead.

The 1H2026 Government Land Sales Confirmed List also adds about 4,600 units, including 635 EC units, which URA says is 50% above the average half-yearly Confirmed List supply over the past decade. That is the policy signal buyers should not ignore.

How Buyers Should Read The Prudence Warning

URA’s warning about prudence is not decorative language. It is aimed at households buying in a period when the macroeconomic outlook is more uncertain, mortgage assumptions may shift, and resale exit plans can be disrupted by future supply. The most useful response is to stress-test the monthly payment before falling in love with the floor plan.

A 0.9% quarterly price rise may make some buyers feel the market is still running ahead. But the same release shows softer launches, a significant pipeline and vacancy data that need to be weighed together. The right question is not whether prices rose last quarter; it is whether your household can hold the property comfortably if interest rates, income or resale timing change.

For sellers, the data cuts both ways. There is still demand, especially in selected non-landed segments, but buyers have more information and may push back harder where asking prices outrun recent caveats. A realistic price is more useful than a headline about the national index.

A Practical Reading Of The Quarter

The final Q1 2026 URA data points to a private housing market that is still firm, but not one where every segment is moving together. Buyers should compare project-level transactions, future supply and financing buffers before committing. Sellers should watch whether nearby launches and completions create competition. The national number is useful, but the block, project and loan details will decide the real outcome.

For the URA Q1 2026 property statistics, the number to keep beside your buying or selling plan is the final 0.9% quarterly rise in private residential prices, not just the direction of the headline. Pair it with URA’s segment data, transaction caveats and residential time series before deciding whether a specific condo, new launch or resale unit is moving with the national index or behaving differently.

Related on Little Big Red Dot: HDB Q1 2026 resale data, COE April 2026 2nd bidding results, Smart Home Tech Show 2026.

Official links: URA Q1 2026 real estate statistics, URA residential time series.

The reader action is project-level comparison. If you are buying, line up recent caveats in the same development or nearby projects, then stress-test the loan against your household income. If you are selling, compare your asking price with actual transactions after the Q1 release rather than assuming the national index justifies any number.