Singapore’s property market showed a tale of two segments in the first quarter of 2026: HDB resale prices notched their first quarterly decline in seven years, whilst the million-dollar flat phenomenon continued to accelerate — reaching an all-time record of 412 transactions in a single quarter.

For homeowners, investors, and prospective buyers navigating one of Asia’s most scrutinised property markets, the Q1 2026 data from HDB and URA offers both reassurance and caution in equal measure.

HDB Resale: A Historic — if Modest — Dip

The HDB Resale Price Index (RPI) fell 0.1% in Q1 2026, the first quarterly decline since Q2 2019 — a span of nearly seven years of uninterrupted growth. The index now stands at 203.4, down fractionally from 203.6 in Q4 2025.

Context matters here. A 0.1% decline is hardly a market rout — it is a rounding error by most measures. But its symbolic weight is significant. The HDB resale market has been one of Singapore’s most resilient asset classes through the COVID years, the global inflation surge, and successive rounds of cooling measures. The fact that it has finally — if barely — given ground suggests that affordability fatigue may be setting in among buyers.

Mature estates such as Toa Payoh, Queenstown, and Ang Mo Kio continued to command strong cash-over-valuation (COV) premiums, particularly for larger flat types. However, transaction volumes moderated somewhat, with buyers becoming more selective as asking prices remained elevated relative to HDB valuations.

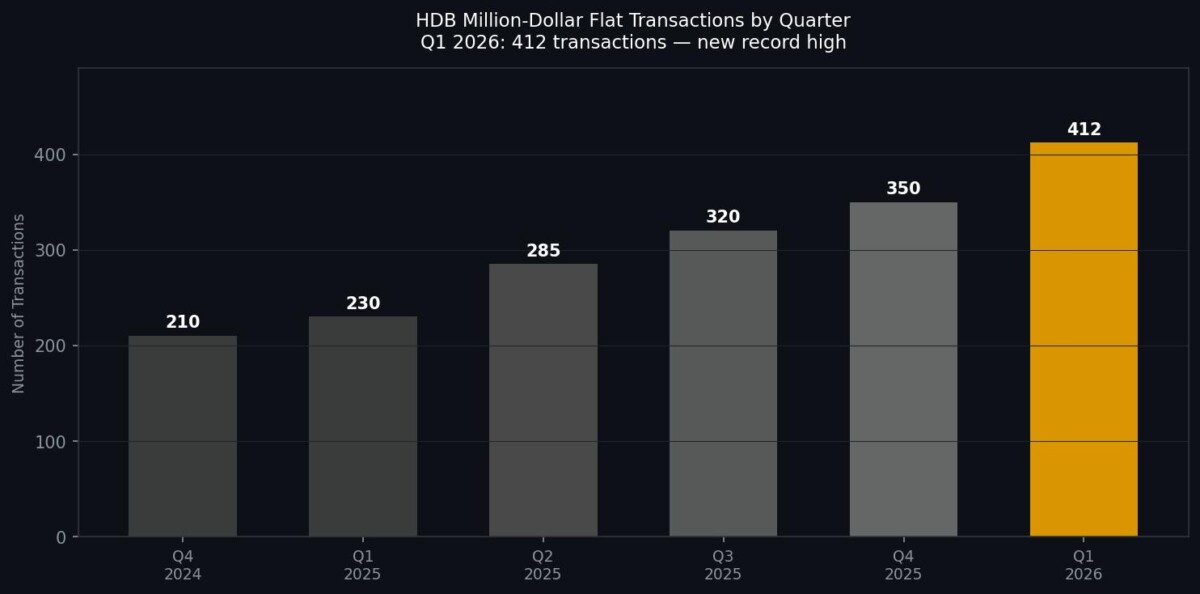

412 Million-Dollar Flats: The Record That Refuses to Stop

Even as the headline price index softened, the luxury segment of the HDB market went the other direction entirely. A record 412 HDB resale flats changed hands at S$1 million or more in Q1 2026 — surpassing the previous quarterly record and cementing what was once considered a curiosity as a permanent fixture of Singapore’s property landscape.

The transactions span a range of flat types and locations, though the bulk remain concentrated in sought-after estates and upper-floor larger units. Notable Q1 2026 transactions included:

- A 5-room flat in Bishan transacted at S$1.38 million — one of the highest prices recorded for a non-DBSS unit

- Multiple executive maisonettes in Queenstown and Clementi crossing the S$1.2 million mark

- DBSS flats in Tampines and Toa Payoh continuing to attract strong buyer interest above S$1 million

For buyers, the rise of the million-dollar HDB flat presents a genuine dilemma. At these price points, the HDB-versus-private calculus shifts considerably — particularly when factoring in the MOP (Minimum Occupation Period), the inability to rent the entire unit during MOP, and the finite lease on the land. Many financial advisers now counsel buyers to carefully model the total cost of ownership across a 30-year timeframe before committing to a seven-figure HDB transaction.

Private Property: Modest Growth, Selective Demand

On the private residential side, the URA Private Property Price Index (PPI) edged up 0.3% in Q1 2026 — the slowest quarterly gain in six quarters. This follows the rapid deceleration seen through 2025, as the Additional Buyer’s Stamp Duty (ABSD) rates introduced in April 2023 continued to weigh on foreign and investor demand.

The Core Central Region (CCR) — covering districts 9, 10, 11, Sentosa, and the Downtown Core — saw the softest performance, with prices essentially flat as high-end demand from foreign buyers remained subdued. The Rest of Central Region (RCR) and Outside Central Region (OCR) held up better, supported by local upgrader demand and the relative scarcity of new launches in well-located suburban areas.

Rivelle @ Tampines: The EC Launch to Watch

The most anticipated new launch of Q1/Q2 2026 is Rivelle, an Executive Condominium (EC) by Sim Lian Group at Tampines Street 95. With approximately 560 units and a location near Tampines West MRT station on the Downtown Line, Rivelle is positioned to appeal squarely to the HDB-upgrader market — the cohort most actively seeking a foothold in private-style housing at below-private-market prices.

ECs remain one of the most compelling value propositions in Singapore’s housing market for eligible buyers. They are priced at a significant discount to comparable private condominiums at launch, yet after the 10-year mark, they are fully privatised and can be sold to foreigners — giving them much of the upside of a private property.

Rivelle’s Tampines location is strategically sound. The estate has historically been one of the strongest performers in the EC segment, given its mature infrastructure, proximity to Tampines Regional Centre and Tampines Mall, and good connectivity to both the city and Changi Airport. Buyers who missed out on earlier Tampines ECs such as The Tapestry and Parc Central Residences will be watching this launch closely.

Income eligibility applies: EC buyers must not exceed the S$16,000 combined household income ceiling, and first-timer applicants receive priority balloting.

What This Means for Singapore Investors and Buyers

The Q1 2026 data reinforces several themes worth keeping front of mind:

For HDB Owners

A 0.1% dip is not cause for alarm — your flat has not suddenly lost value. But it is a signal that the extraordinary run of resale price appreciation may be moderating. If you are considering selling in the near term, the current environment still supports reasonable valuations, particularly for larger units in mature estates. Timing the market perfectly is rarely possible, but waiting for a significant rebound from here may not be the most productive strategy.

For Prospective HDB Buyers

A softening RPI, combined with the government’s continued supply of Build-to-Order (BTO) flats — including under the new PLH (Prime Location Housing) and Plus models — means buyers have options. If you are considering resale, negotiate firmly. COV expectations from some sellers remain elevated relative to where the market is heading, and there is growing room to push back.

For Private Property Investors

The slowdown in the URA PPI growth rate (from ~1–2% quarterly gains in 2024 to just 0.3% now) suggests that the easy gains in Singapore residential property may be behind us for this cycle. Investors who entered pre-2022 are sitting on healthy gains; those entering now should have a longer holding horizon and realistic return expectations. The S-REIT market — which offers exposure to Singapore commercial and retail property — may warrant more attention for those seeking yield rather than capital appreciation.

For EC and New Launch Buyers

Rivelle represents good value for eligible buyers at current pricing expectations. EC launches in well-connected suburban estates have historically sold out quickly, and Tampines has particularly strong demand fundamentals. If you are eligible and in the market, this is one to research seriously. Use CPF OA savings strategically, and factor in the 5-year MOP before re-sale, and 10-year mark for full privatisation.

The Bigger Picture

Singapore’s property market remains one of the most policy-managed in the world. The government has repeatedly demonstrated its willingness to act — whether through ABSD hikes, loan-to-value tightening, or supply adjustments — to prevent runaway speculation whilst maintaining a broadly stable market for owner-occupiers.

The Q1 2026 data suggests those interventions are working as intended: private price growth has slowed to a crawl, HDB resale has finally nudged lower, and yet there are no signs of a sharp correction. For long-term resident-investors, Singapore property remains a store of value — not a get-rich-quick vehicle, but a reliable, policy-supported asset class in a city-state with severe land constraints and continued population demand.

The million-dollar HDB story, meanwhile, is a reminder that even public housing in Singapore has become an asset class of its own — one that demands the same rigour of analysis as any other investment decision.

This article is for informational purposes only and does not constitute financial or property advice. Readers should conduct their own due diligence and consult a licensed property agent or financial adviser before making any investment decisions.